The Mortgage Sales Process That Wrote £1.1m in a Year

The two-appointment method: fact find first, sign up second. How four brokers combined wrote over £1.1 million using one simple structure.

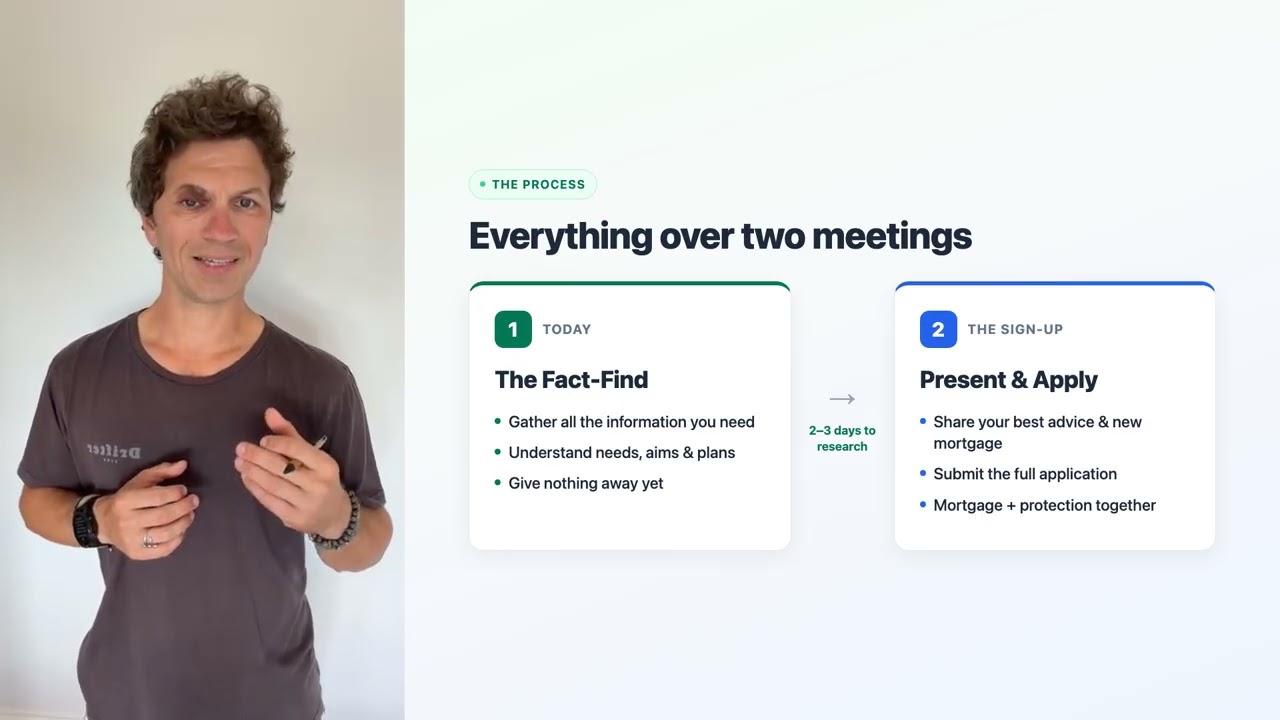

Why split it into two appointments?

A lot of brokers try to do everything in one meeting. Fact find, research, recommendation, application, protection. All in one sitting. It feels efficient but it doesn't convert well, especially with colder clients who came through an online funnel or a booked appointment rather than a warm referral.

The two-appointment process solves a specific problem: it stops you giving the client something to compare before you've done the work.

If you discuss rates in the first meeting, even roughly, the client leaves with a number in their head. They scroll the internet that evening, find a rate that's 0.01% less than what you guessed, and they go elsewhere. You never hear from them again. I've seen this happen to experienced brokers who should know better.

Splitting it into two meetings means:

- Meeting one (the fact find): you gather all the information you need. You understand the client's situation, aims and plans. You give nothing away about rates, products or outcomes.

- Meeting two (the sign-up): you present your recommendation with full research behind it. You share your screen, walk through the options, get the client's agreement, and submit the mortgage and protection applications live.

The gap between the two meetings is two to three days. Enough time for you to do thorough research. Short enough that the client stays engaged.

The numbers behind this process

In 2021, myself and three other brokers wrote in excess of £1.1 million in mortgage and protection business using this exact method. One broker alone wrote in excess of £365,000 in a year purely from remortgage business. The biggest years were after COVID, when all appointments were done remotely and over the phone.

In the firm I used to work for, we knew many brokers who were easily writing in excess of £250,000 a year, and a handful were doing over £300,000 to £350,000 a year using this process. These aren't outliers. They're brokers who followed the two-appointment structure consistently.

My brokers at Bluewave run the same process today with appointments booked through MortgagesBooked. The appointments are booked in the same way and the process converts them the same way.

Meeting one: the fact find

The client is expecting a full fact find. These are not quick five-minute chats to book them in at a later stage. They've been primed to have documents ready: payslips, knowledge of outgoings, mortgage statements.

The first thing you do is lay out the process. Explain clearly:

- "Everything is done over two meetings." The first meeting is for you to gather all the information you need, understand their needs, aims and plans.

- "I'll book a second meeting within the next two to three days." That gives you enough time to do your full research.

- "In the second meeting I'll run through exactly what I consider the best advice and the best new mortgage for you." That's when you get the process started and submit the full application for mortgage and protection.

Setting this up front is important. The client knows what to expect, they know there's a second meeting, and they're not waiting for you to pull a rate out of a hat.

The critical rule: don't discuss rates

At no point during the first meeting should you discuss interest rates or what the potential options could be. If the client pushes for it, resist. Even if you know exactly what the outcome will be, move the recommendation to the second meeting on 100% of cases.

If you give them a rate, you give them something to compare. They will compare it. And if someone else quotes 0.01% lower, you've lost them.

This is the single hardest discipline for experienced brokers. You know the answer. You want to be helpful. But saying it early loses more clients than it wins.

Between the two meetings

Once the fact find is done, you book the second meeting before ending the first call. Two to three days out. Then you do your work:

- Run your full sourcing and product research

- Prepare your recommendation

- Get your compliance right

- Prepare any protection quotes you plan to present (the conversation itself is covered in how to sell protection to mortgage clients)

- Have everything ready to submit live in the second meeting

The gap also builds anticipation. The client has committed their time, shared their financial details, and is now waiting for your professional recommendation. That's a much stronger position than trying to close someone who's hearing everything for the first time while still being asked for their national insurance number.

Meeting two: the sign-up

We call the second meeting "the sign-up" because that's what it should be. This is where you present your recommendation, get agreement and submit the application.

Always do this over a video call. The reason is simple: you need to share your screen. In this meeting you're walking the client through:

- The mortgage recommendation and why it's suitable

- The documents on your system (European Standardised Information Sheet, key facts)

- Protection recommendations (life insurance, income protection, critical illness)

- The client's agreement to proceed

- The live application submission

- Any life insurance medicals, which you can complete with the client watching your screen

Doing this over a phone call without screen sharing is harder for the client to follow and harder for you to convert. When they can see what you're doing, they trust the process more and the sign-up happens naturally.

Before the appointment starts

We have automations in place before the first meeting: emails and text messages that remind the client and try to gain their commitment to join. Some brokers want to reach out to the customer beforehand, but be aware that this gives them another chance to cancel.

My brokers and I do not contact the customer at all before any of our meetings. We let the automations do their thing. If you're new to this process, I'd recommend the same. Only start reaching out once you're confident and comfortable. For now, trust the system.

Why experienced brokers sometimes struggle with cold clients

Some of the most experienced brokers out there, years of doing the role, struggle with platforms like MortgagesBooked or similar appointment-based leads. I've seen it, and the reason is always the same.

They're used to referral clients. Estate agent introductions. Existing customers coming back. Warm people who already trust them before the conversation starts. The rapport is half-built before they pick up the phone.

A client from a social media funnel or a booked appointment is different. Yes, they've taken time to complete 17 or 18 different questions and they've booked a meeting. But to you and your firm, they're still a new customer. The trust isn't there yet. You have to build it.

The two-appointment process is specifically designed for this. The fact find builds trust through professionalism and thoroughness. The gap builds anticipation. The sign-up converts through preparation and screen-shared transparency. It works with cold clients in a way that winging it on a single call doesn't.

I covered the scripts and follow-up cadence separately in mortgage lead conversion tips. This post is the structural framework those scripts sit inside.

All I can say is trust the process. Two appointments. The first is the fact find, gather everything, give nothing away. The second is the sign-up, share your screen and go through the recommendation. It will work for you.

If you want to put this process to work with pre-qualified, booked appointments, the free preview shows this week's available meetings. And for the call scripts and 30-day follow-up cadence that sit alongside this structure, read mortgage lead conversion tips.